With a glance to the future Comms Business Magazine reviews the current activity from the major headset vendors and their distributors to establish the trends in the market and provide some sales tips with which to generate extra margin.

The future for the headset market looks very exciting when you factor in newer technology coming through from the consumer market. Thetrend towards wearable technology is certain to deliver new ways of working and new applications to the headset market just as consumers, by way of bringing their own devices in to the workplace, have influenced business practices.

The wearable technology market is in the midst of a boom and shows no signs of slowing down. Deloitte recently revealed that it expects the industry to generate $50 billion by 2018, and predicted that over 100 million wearable devices will be in use by 2020.

Plantronics observes that the roots of this market can be traced back to a device that has for years provided intuitive hands-free functionality to businesses, the headset and says that today, forward-looking vendors are looking beyond traditional audio functions and entering a world of contextual awareness in which their devices better understand their users.

Already the vendor is integrating sensors and software that can anticipate users’ needs into their products. With these additions, headsets can factor where people are and what they are doing into how they operate to proactively deliver a more intuitive user experience. These devices can increase productivity by automatically answering calls, and help improve data security by proactively locking wearers’ PC screens whenever they walk away from their computers.”

Paul Dunne, Head of Channel Sales commented, “The headset industry is an exciting place to be at the moment. One of the biggest technological developments we’ve seen is the ability of new headsets to connect with two or three devices at once, and to automatically update their wearers’ UC presence on Microsoft Lync and Skype whether they are on a PC or mobile call. With many people now working with multiple technologies simultaneously, keeping them connected to the system no matter which of these they are using has become critical for businesses. In response, headsets have begun adapting to connect with a wide range of technologies, including soft phones, smartphones, tablets, and gaming consoles.”

As headsets become more intuitive and more closely integrated with software, the stage is set for developers to get involved in the innovation process and customise products to address the needs of specific businesses.

Market Trends

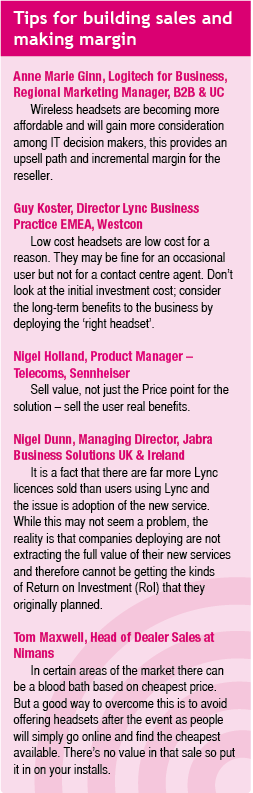

Whilst we may all eagerly await these new developments and the opportunities for sales they will create we have today a vibrant market for existing products as Guy Koster, Director Lync Business Practice EMEA at Westcon comments.

“Over the last year Westcon has experienced exceptional growth in its headset business as demand for headset devices has soared, resulting from increased use of Unified Communications and Collaboration solutions from vendors including Microsoft, Polycom, Avaya and Cisco. Due to the exponential rise in the use of mobile devices (particularly smart phones and tablets) the addressable market has also grown significantly.

Headset device vendors also report that growth from their portfolio of professional UC&C devices is typically twice that of their average growth, confirming that the headset category is the fastest growing in the UC market.

Historically, businesses would typically invest in a UC solution without budgeting for headsets that are necessary for a reliable, high-quality deployment. Acquiring low-cost, low-quality devices at the last minute can compromise the quality of the users’ experience, and would often result in a business being unable to realise the full anticipated ROI from their investment in the UC solution and the IT Department being blamed for inadequate performance. Businesses are now realising, with guidance from the channel, that the ‘last three feet’ - the space between the users’ device and their ear – is the most important, in the sense of maintaining the quality of the UC experience from the users’ perspective. Evolving changes in procurement policy, with responsibility for decision making moving away from the IT Department and into Line Of Business stake holders is changing the rules and businesses can now begin to harness the collaborative benefits of their chosen UC solution by planning for the costs of headsets in advance and within their overall UC budget.

Major headset vendors are also working closely with vendors such as Avaya, Microsoft and Cisco to ensure their headsets are optimised to provide the best possible user experience.”

Nigel Holland, Product Manager for Telecoms at Sennheiser, says that in terms of the market drivers, there’s one factor that is bigger than anything else – adoption of Unified Communications technology.

“UC is by far the biggest driver of professional communication UK headset growth with estimated headset attach rates at least reaching 60% per active endpoint compared to 5% for a desk phone. The general consensus in the headset industry is that by 2016, UC headset revenues will account for at least 50% of the available market.

Why this growth? Well, laptops and desktops when not assisted by a headset or similar peripheral communication device are not optimised for telephony, which can often result in a poor quality call experience.

As a parallel trend, we’re also seeing a strong migration to wireless headset solutions, with a rise in the use of wireless devices from 8% in 2009 to 40% in 2011. Current wireless adoption rates are even higher and now account for approximately 50% of total revenues across the professional communication headset category. In particular we have seen a significant rise in adoption at contact centres, previously a bastion for corded headsets. This is a very significant market in the UK with presently over a million dedicated contact centre workers.”

Nigel Dunn, Managing Director for Jabra Business Solutions UK & Ireland, has seen that Unified Communications has become more prevalent in the last 12 months, with customers moving on from pilot stage into full deployment, as they make decisions to invest in the technology.

Nigel Dunn, Managing Director for Jabra Business Solutions UK & Ireland, has seen that Unified Communications has become more prevalent in the last 12 months, with customers moving on from pilot stage into full deployment, as they make decisions to invest in the technology.

‘We are therefore seeing these deployment accounts investing predominately in mid-range corded headsets. This implies that customers now understand that the quality of the audio device selected is integral to the overall implementation and how they can be instrumental in making or breaking a successful deployment, whilst more importantly, being key to encouraging wide-scale adoption.”

James Burns, Business Unit Manager – UC Devices at Exertis Micro-P says that the Contact Centre and Office market is still a core area for them and their partners.

“The adoption of wireless technologies in the traditional CC & O space continues to increase. Our headset portfolio is now labelled the CCU&O portfolio to reflect the rise in the adoption of multi-purpose UC headsets. These are channelled through not only our traditional voice partners and headset specialists, but our upturn in this area reflects how the IT VAR channel has adopted and continues to adopt voice technology. As end users are rationalising their supply chains, this is inevitably reflected right throughout the supply chain to distribution and vendor level where our partners are looking for a single distributor to facilitate all their technology requirements. Exertis Micro-P’s extensive range of products and technologies allows our partners to do just that, from Networking and infrastructure to Mobile and UC End Points and Headsets.”

Tom Maxwell, Head of Dealer Sales at Nimans, is also seeing a strong and continuing theme towards UC and the Lync effect.

“There’s more and more adoption which is driving demand for optimised headsets. The end point is too often viewed as the last piece of the jigsaw and overlooked which is dangerous as it’s one of the most important factors to maximise audio performance and the user experience. Dealers are definitely getting in on the act and recognising that a headset has somewhat migrated in recent years. It’s now being viewed as an IT solution, not just a voice-based product. Many of the biggest orders are UC related.”

Is there a VoIP/Lync Effect?

Microsoft has seen quarter over quarter growth in its Lync business in excess of 30% over the preceding 5 quarters evidencing the fact that Lync is the fastest growing UC solution in this market category. As further evidence of acceleration in adoption of Lync as a business’s primary voice solution, respected industry analyst MZA recently reported that Lync is now the number three PBX vendor in North America. Jerry Caron, an analyst with Current Analysis also noted that ‘Microsoft has gone from nothing to third in two to three years. It’s become a very significant player in a very short period of time’.

Guy Koster

Guy KosterGuy Koster at Westcon, believes that voice is a fundamental workload within the Lync solution – and provision of high-quality headsets within a deployment enable users to truly harness the power of voice and audio that can deliver the ‘full’ Lync experience.

“In a Lync deployment, the voice functionality can be enabled either using the Lync soft client or through an Ethernet or USB connected desktop handset that is Lync Optimised or Qualified in conjunction with a headset.

Discussing device selection at the initial planning stage of a Lync roll-out is critical – creating pilot groups profiled around different worker types is now considered ‘best practice’ to ensure appropriate devices are selected which best fit the group’s needs. When workers become familiar with using headsets (in conjunction with the Lync client or desk phone), there is a higher likelihood that the ‘full’ benefits attributable to a Lync deployment can be achieved by adopting a headset device

Anne Marie Ginn at Logitech for Business agrees when she says, “Absolutely. The economic recession of the last few years delayed companies plans to deploy UC clients in many cases, however with the economy turning around, there is a pent-up demand, and the market is forecast to grow double-digit for the coming years. The question is no longer whether to go VoIP or UC, it’s when, and increasingly companies are looking at hosted or cloud-based UC for increased cost-savings and flexibility.”

Nigel Dunn at Jabra is starting to see a VoIP/Lync effect, although he says it is currently still a slow-burner.

‘Voice applications are now beginning to be deployed, which will supplement the headset market with demand from these users, many of whom are new to the category as they previously haven’t used headsets with their deskphones. This transformation in workplace voice applications will drive mainstream headset adoption that in turn will reveal productivity and mobility gains and unlock the true benefits of UC, thus maximising infrastructure investment to order to deliver ROI.

An example of the Lync effect is positively emphasised by sales of Lync-optimised devices. We have seen 100% YoY growth of this particular SKU across our portfolio in 2013 versus 2012 and are therefore confident in predicting further implementation of these variants in 2014 and beyond. This has been driven by Lync being relatively unique in that it almost pushes companies to use softphone only, which means that headsets are mandatory. It helps save space on desks but headsets allow the user to freely interact in the new media-rich environment that Lync creates.”

As an aside, and in a nod to our business market consumerisation trends noted earlier Dunn says, “Another driver in general headset adoption is the consumer trend in audio headphones usage, removing the stigma around wearing a headset and turning it into a symbol of a more device/tech-savvy individual.”

James Burns at Exertis Micro-P says that Enterprise Voice rollouts are key for the distributor and their partners, with Cisco Jabba and Microsoft Lync as the core drivers.

“The most successful of our partners are those acting as a trusted advisor for all technologies. This is where Exertis MicroP steps in to support our reseller community with our in-house CCU&O expertise, helping to ensure our partners are not only capitalising on all sales opportunities, but more importantly, offering the right solutions most appropriate for each end user profile. For example, across a Lync or Jabba rollout, you could be looking at 5 or 6 different end user profiles, from the contact centre worker, through to the mobile road warrior - each of which requires a bespoke headset solution to fulfil their needs.

Lync, Jabba and Avaya One-X have created the need to refresh an end user’s traditional headset estate. The isn’t just a case of upgrading a phone system, increased softphone applications have generated the need to adopt a fit-for-purpose headset solution based upon the end-user’s profile. Ever-changing, more flexible ways of working demand multi-connectivity devices and UC end points. For example, whether I’m hosting an internal tele-conference with my team from the office, or speaking to my FD about an investment whilst travelling on the train, I expect the same user experience for myself and the other caller as if sat in my office using a traditional headset solution for my deskphone.

Complete headset estate refreshes occur when a solution such as Lync is adopted for enterprise voice – effectively a rip and replace of the end user’s communications platform. However, the reality is that end users will pilot a new solution such as Lync running it parallel (with limited functionality) with their existing solution such as a traditional PBX. This makes the need for a multi-connectivity headset solution an absolute necessity. Models such as the Plantronics Savi Wireless range of headsets and the MDA 200 communications hub allow users to switch seamlessly between multiple voice applications as well as transitioning to a UC headset whilst using their existing infrastructure.”

Burns concludes, “As the way in which we work continues to evolve, as does the technology we need to use. Plantronics have every platform, system and end user profile catered for.”

Tom Maxwell

Tom MaxwellNimans Tom Maxwell says Lync is slowly filtering down to the SMB.

“I was with a traditional PBX reseller recently and they are now selling Lync. A lot of the voice resellers are evolving and moving with the times on a weekly basis. However others still don’t fully understand what Lync is so as an industry we need to educate them more and this is an area Nimans is focusing on.”

Myth Busters!

David Whitehead from Headsets4Business believes many dealers are missing out on extra margin simply through neglect or due to failing to ask the right questions

“Neglecting the opportunity is largely down to two perceptions. The first is headsets are complicated, lots of different leads and many types of headset, and it’s easy to supply the wrong product. Secondly headsets have become commoditised and therefore the margin just isn’t there.

Both these perceptions are myths, a headset sale is remarkably simple, and if you supply the right product dealer margin is very good.

After neglect, failure to ask the right question is the major mistake. Simply asking your customer or prospect if he or she needs or wants any headsets just doesn’t cut it. The questions you ask need to be discussion provoking and you need your customer to departmentalise their business when you discuss headsets. The obvious benefits of health and well-being and increased productivity will be the deal makers, and the departments that will benefit the most will become clearly apparent. We work closely with partners so they understand which questions to ask in order to make the sale.

In addition, it’s important to know when to ask the questions, and with our proven strategy you get three bites at the cherry. Relevant questions about headsets should asked pre sale, at point of sale, and if necessary post sale (project management stage)

Asking the correct question at the right stages of the process will achieve great results. You have to integrate this into your overall sales process. So if you are primarily selling a telephone system, headsets become a natural part of the process.”

Whitehead adds, “Dealers want to know how much extra margin they can make by adding headsets to their portfolio. Research done with our resellers tells us an average profit return on a telephone system sale is circa £80.00 to £100.00 per extension. Profits of at least £20.00 per headset (even on an entry level wired headset) are achievable. So if a dealer sold a headset with every extension (an extra £20 profit per extension) their margin would increase by 20% - 25%. If they supplied headsets for half of the extensions they would make an extra 10% - 12.5%.

Multiply this extra margin across your annual system sales, and combine this with the opportunity to sell into your existing customer base, and you will have a serious increase in profit. So don’t miss out, because if you do you can be assured that someone else is selling headsets to your customers.”

Ed Says…

We are going to see a shift in the future for headsets. If headsets are successfully integrated in to the huge boom in wearable technology we are seeing right now then with the right applications to grasp user attention the market for ‘smart’ headsets could explode from the home in to the work place. Watch this space…